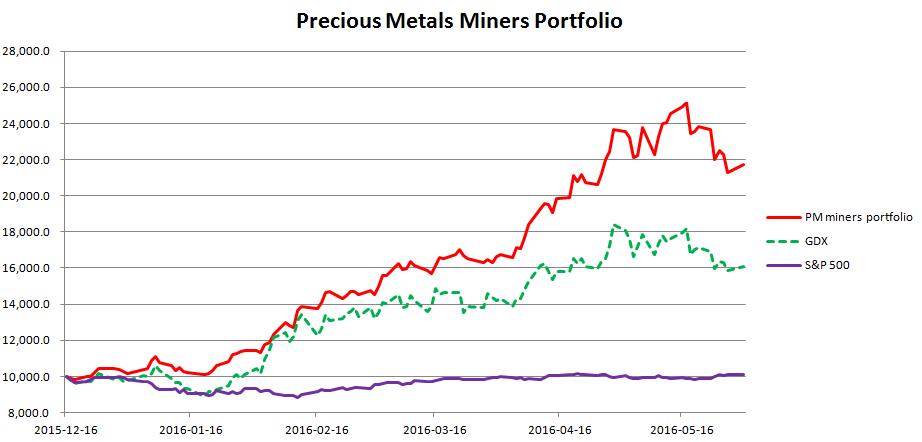

Impairments

Although in 2015 Newmarket Gold made higher profit from mining operations ($60.6 million versus $41.3 million in 2014), the company printed a net loss of $2.8 million (in 2014 Newmarket made net income of $20.0). Let me comment on this issue.

In its 2015 report the company stated (page 25):

"At December 31, 2015, the discounted cash flows over the life of mine for Cosmo was below the carrying value of the long-lived assets of the mine and as a result an impairment of $24,073 was recorded against mine properties and $1,424 recorded against property, plant, and equipment (Note 16), resulting in a total impairment charged to the statement of operations of $25,497"

This impairment charge accounted for the largest part of the total impairment charges, recognized in 2015 ($26,499 thousand in total). In 2014 the company did not recognize any impairment charges. Quite contrary, Newmarket recovered $8,359 thousand from impairment charges recognized in earlier periods. So the results reported in 2015 were worsened by $34,858 thousand, when compared to 2014. In other words, the accounting rules "artificially" lowered 2015 results by $34.9 million. It means that, on a comparable basis, Newmarket would have made a net profit of $32.1 million in 2015 (61% higher than in 2014).

I am writing "artificial loss". Well, I do not claim that accounting rules are worth nothing. Quite contrary. They are very useful because the investors know the actual financial situation of a company.

However, in the gold mining industry a majority of impairment charges are applied when gold prices are much lower than in previous years. With lower gold prices the value of a gold deposit is lower in the long - term. Why? Because there are less ounces of gold which are economically viable. And less ounces of gold means lower revenue in the future and lower value of a deposit.

However, if the prices of gold go higher, the previously recognized impairments will be reversed. So be cautious with impairments - it is a very useful tool but, as any tool, it has to be applied thoughtfully.

Next thing - Newmarket Gold applies very conservative assumptions when determining the recoverable amount of its mines. Let me cite the company, once again:

"For the determination of the impairment, a gold price estimate of A$1,550 per ounce was used for 2016 through 2018, and A$1,500 for 2019 and beyond, taking into account the impact of the Australian dollar exchange rate on the US dollar and using an average Australian dollar foreign exchange rate of $0.75 over the period. A discount rate of 12.5% was used to present value the estimated future cash flows from the operation"

Today A$1,550 is equivalent to US$1,172. It means that the company assumes the medium-term price of gold of $1,172 per ounce, while today gold is trading at $1,250 per ounce (6.6% higher). It means that there is quite a high probability that the company's gold price assumption may be deeply underestimated.

The same thing is with the discount rate of 12.5% - in most cases a rate in the range of 5% - 10% is applied. A discount rate which is higher than usually means underestimation of the impairment charge.

Summing up - while, in my opinion, it is reasonable to use conservative assumptions when calculating recoverable values, the investors should understand how these impairments are calculated.

In the case of Newmarket Gold investors should keep in their minds that impairments charged by the company may be deeply overstated.

Mineral Reserves

There are no current estimates of Newmarket Gold mineral resources / reserves. The last estimates were reported at the end of 2014. According to these estimates:

As the table shows, the company reported relatively low mineral reserves. I remind to my readers that currently Newmarket has three active mines: Fosterville, Cosmo and Stawell. The chart shows that all these mines had 637 thousand ounces of gold classified as mineral reserves. It was equivalent to only three years of mining.

However the strength of this company lies in its resources and the ability to convert resources to reserves. The table below shows mineral resources held by Newmarket Gold at the end of 2014:

Again, at the end of 2014 Fosterville, Cosmo and Stawell were holding mineral resources of 2,932 thousand ounces of gold, which was equivalent to 13 year of mining. The problem is that resources are not that part of a mineral deposit, which is economically viable. To be economically viable, resources must be converted into reserves. To do it, the company must invest, for example in additional drilling, In 2015 Newmarket Gold spent around $12 million on exploration and $42.9 million on development of its properties. I believe that the company will publish an update to its mineral base estimates very soon.